The Home Loan Process

Demystifying High Rates for Home Buyers

When buying a home, high interest rates can feel intimidating. The good news is that rates can change, and you can strengthen your position by maintaining a solid credit score, steady income, and manageable debt. A higher rate today doesn’t always mean you’ll pay more over the life of your loan. Options like refinancing down the road or making extra payments can help reduce the amount of interest over time. That’s why it’s so important to work with a trusted lender who can walk you through your options and help you find the best path forward. If you don’t already have a lender you love, we’re always happy to recommend trusted professionals who will take great care of you.

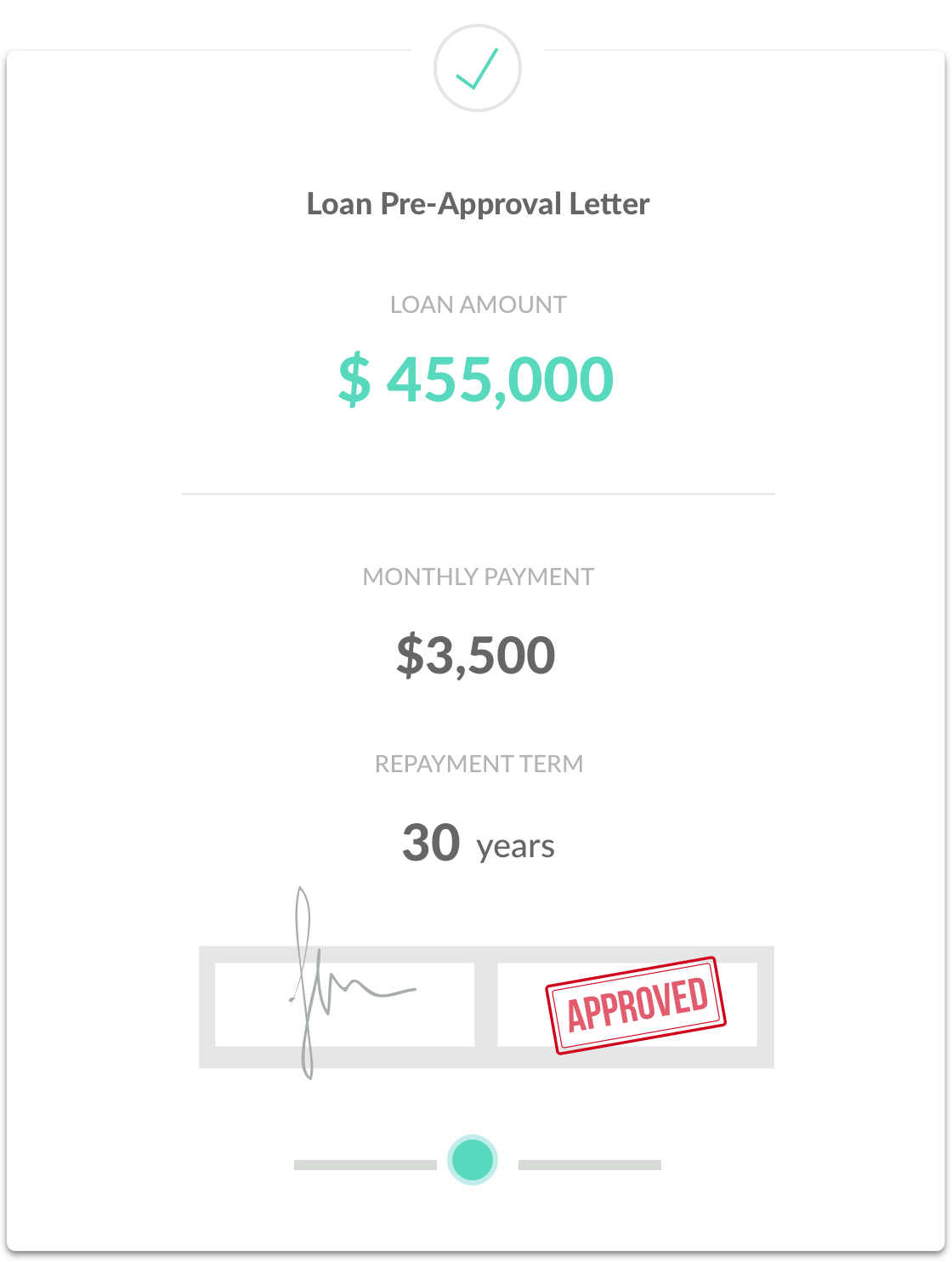

Get Pre-Approval

Before starting your home search, it's a good idea to get pre-approved for a loan amount with a lender. The lender will gather information about your income, assets, and debts to determine how much house you may be able to afford. This includes reviewing your credit report, W-2 forms, pay stubs, Federal Tax Returns, and bank statements. There are a variety of different loan programs available, so make sure to get pre-qualified for the specific programs that best suit your needs. By getting pre-approved, you'll have a better idea of your budget and be able to move forward with your home search with confidence.

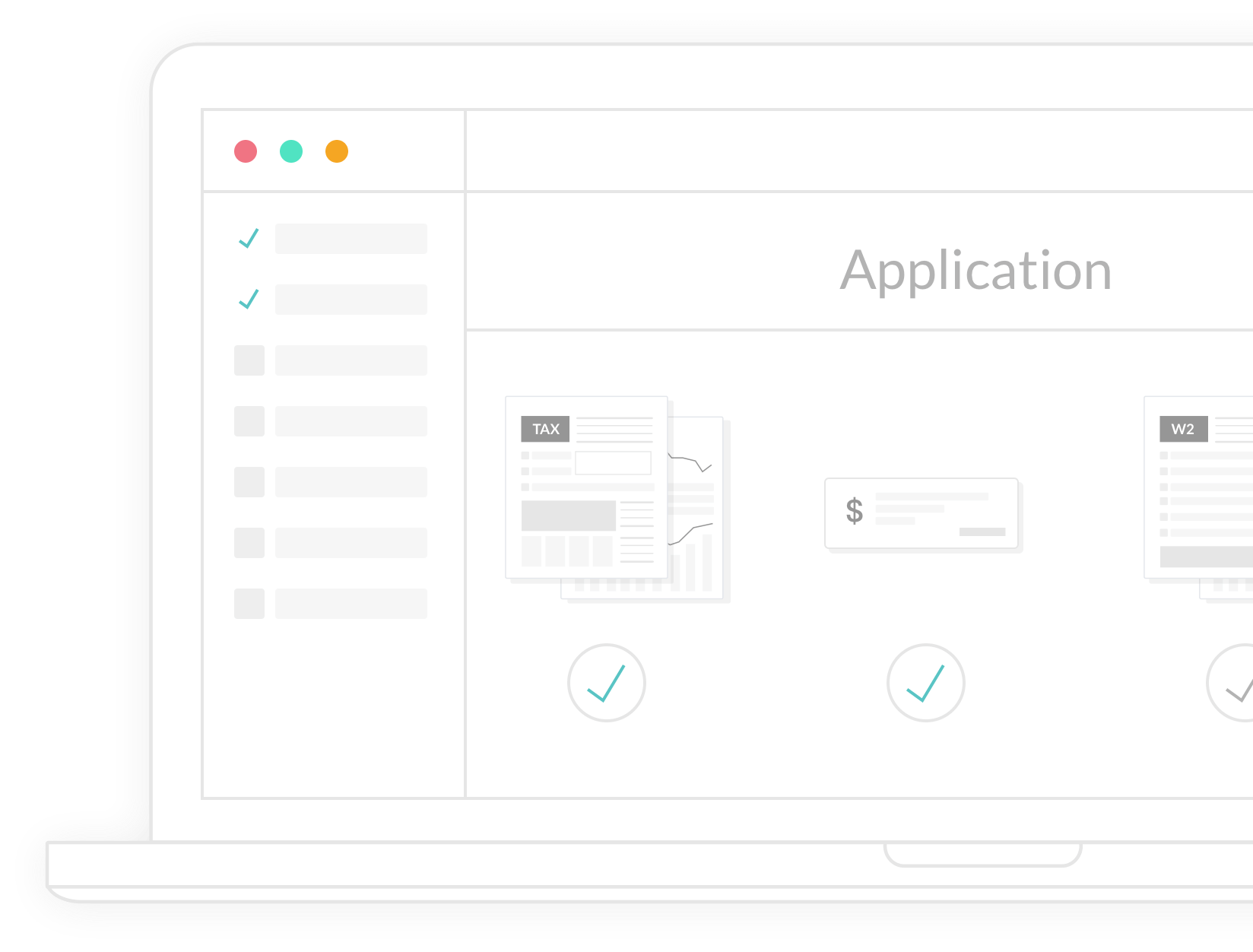

Application & Processing

What happens when a loan goes "live"

When you're ready to buy a property, your lender will assist you in completing a full mortgage loan application and discuss the various fees and down payment options. Once submitted, the application is processed, and the documents are reviewed, appraisals are ordered, and title examination is conducted. The loan is then sent to an underwriter who will carefully review and approve the entire loan if it complies with the necessary requirements. Your lender will guide you through this process to ensure a smooth and successful home buying experience.

Closing

Signing and Finalizing the deal

It's important to be prepared for additional documentation or clarification requests throughout the loan process. Once your loan is approved, don't forget to secure homeowners insurance. Your loan documents will be sent to the title company, where you'll sign for the new home and pay any remaining costs. After that, the loan will be recorded, and you'll finally get the keys to your new home! Congratulations, and welcome to homeownership!